To operate efficiently we must use our existing resources to create greater value. However, to measure this value and the success of our efficiency drive, we must first establish baselines against which we will measure that success. The ultimate aim is to be able to use the same resource base to add greater value and impact while lowering the costnd effort of creating that value.

Establish the organisation’s productivity and efficiency baselines

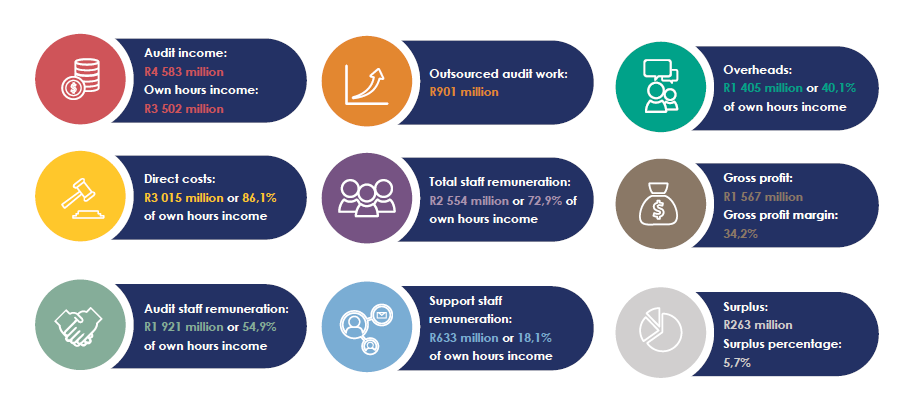

For this assessment we used the concept that productivity equals creating value. Increased productivity results in creating more value with the same resources or creating the same value with fewer resources.

The AGSA’s total productivity (output) is a result of many interlinked factors and a reflection of our business model. The business model processes include our practices to optimise efficiencies in the people, processes, systems and capital (tools) areas.

Depending on the focus of the work, we have established various productivity and efficiency baselines. The overall productivity baselines include:

Analysis of the audit process

For the audit efficiency baseline, we looked at the audit process based on the AGSA’s audit methodology, and rated inefficiencies and areas that would benefit from automation.

Overall, we reviewed 99 working papers of which 48% were found to be good candidates for automation and will be built into our customised audit software. Data points will be integrated across all business units that use these specific working papers.

Business efficiency baseline

We approached the establishment of the business efficiency baseline by investing in the development of a business process assessment framework with the conviction that a formal description and quantification of each business process is the best way to identify areas for improvement or automation.

While the main driver for this work is to minimise capital investment, time and resources, these are not the only factors that will be applied to a decision. At times, these drivers will show a negative return on investment but a strategic imperative will still require investment, such as digitisation to prevent reputational damage.

The process assessment framework was applied to the daily deposit process in the Finance business unit. The resulting business case demonstrated the viability of the investment in the automation of this process which in turn resulted in the deployment of the first robot in our organisation.

The net present value of the automation of the daily deposit process over 60 months is expected to be over R1,6 million, or 20-times the improvement in speed and over 2 000 hours reduction annually. It will also significantly decrease the risk of misallocating deposits.

The next step is to form a productivity committee to track the improvement in overall productivity. The committee will also support or sponsor further research and analysis of matters related to productivity as the need for deeper or specific understanding arises.

Conclusion

Developing a comprehensive view of our resources and how they have been spread and used throughout the business was a first step towards identifying how and where to achieve productivity, audit and business efficiencies. However, with these efficiencies comes change.

An organised system’s productivity is a reflection of the organisation’s business and operating model. To improve our efficiency and achieve significant changes in our productivity we will have to review our operating principles.

These include important systems of operation such as business units vs delivery centres, delivering value vs billing per hour, and blending human and technological resources vs human resourcing using tools.

Eventually, it will be important to redefine the productivity baselines for a business model that moves away from charging audit fees based on hourly rates and presence at the office activities.

While major changes in the business model might take place over a longer time, we must continue with incremental improvement to productivity as a normal business practice.