Public sector institutions play a key role in delivering services, driving overall government programmes, and overseeing a substantial portion of the public purse. All these have a significant impact on the lives of citizens. As public sector auditors, we have committed to using our #cultureshift2030 strategy to provide strategic and informative insight, drawn from our audits, to enable government to take the right decisions and have a meaningful impact on the lives of citizens.

Analysing the trends in these audit outcomes helps to spark understanding and a commitment to act from all the roleplayers in the accountability ecosystem, as was done in the national, provincial and local government general reports.

General reports

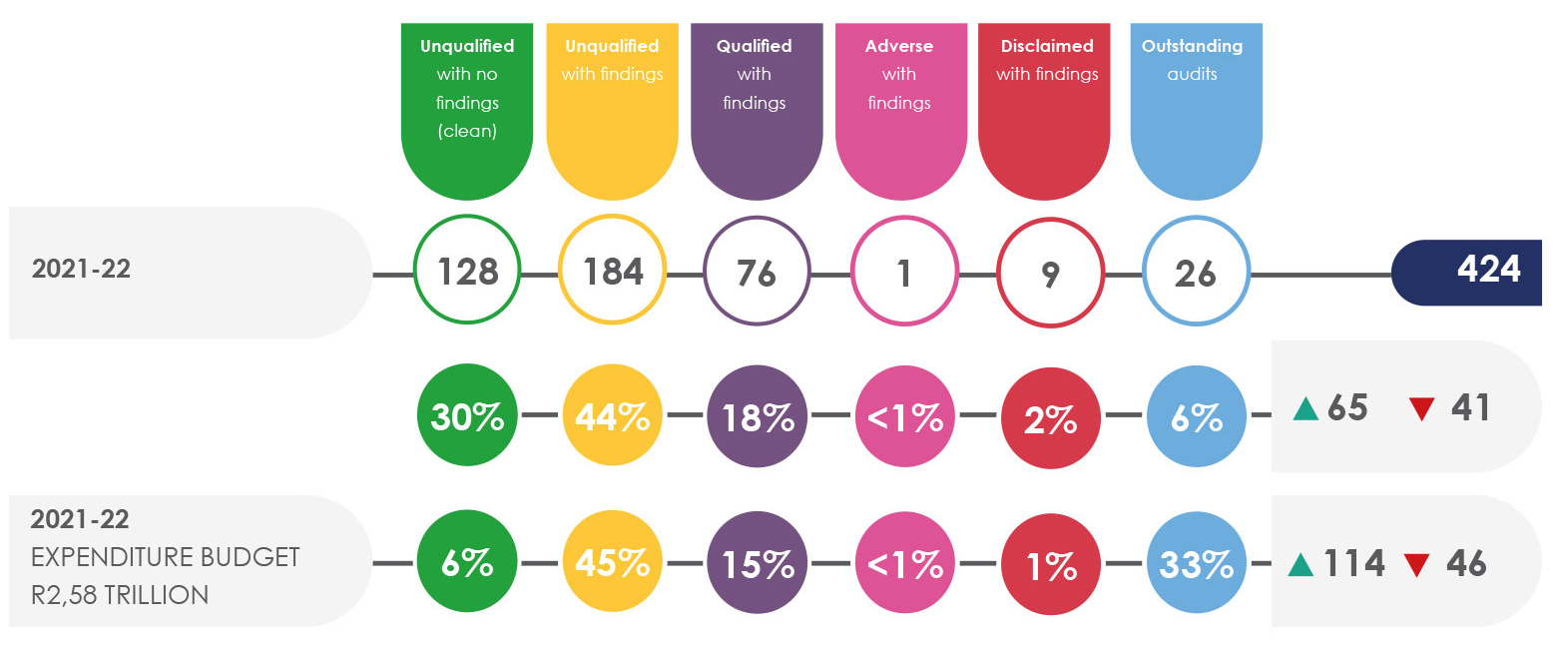

Our general reports serve as a state-of-governance account of how our government – at all three tiers – has spent taxpayers’ money during a particular period. We tabled two general reports during 2022-23.

As a result of rigorous scrutiny of the accounting records and other related information to support financial statements and performance reports of auditees, both general reports provide a comprehensive analysis of the audit outcomes and represent the main source of insight into the stewardship of public funds in the country.

The reports are rich in statistics and real examples on the state of the audited entities, with a particular focus on key service delivery mechanisms. The value of the reports is rooted in the use of the information they present, hence, to drive culture shift and improvement in the public sector, we specifically detailed recommendations.

Audit outcomes

The audit outcomes showed a gradual upward trend since the term of the previous administration ended. We acknowledge the effort and attention that has been paid to improve the basics of financial and performance management and the disciplines that underpin a good audit outcome, especially a clean audit.

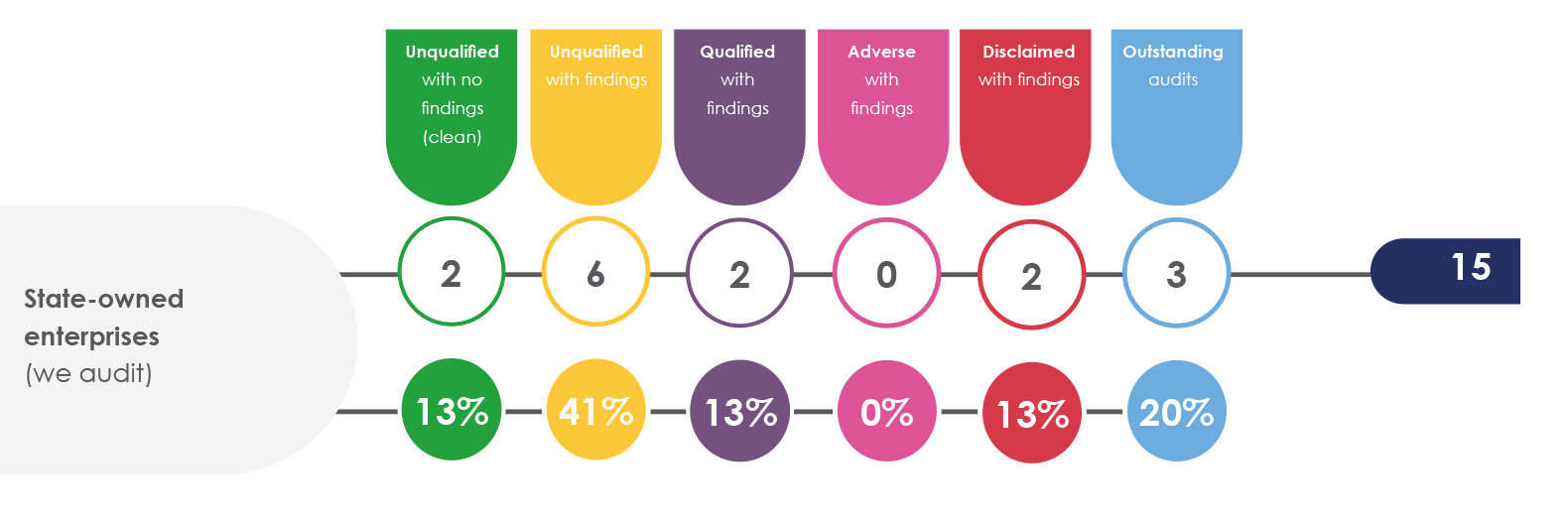

Audit outcomes of state-owned enterprises (excluding subsidiaries)

Audits outstanding

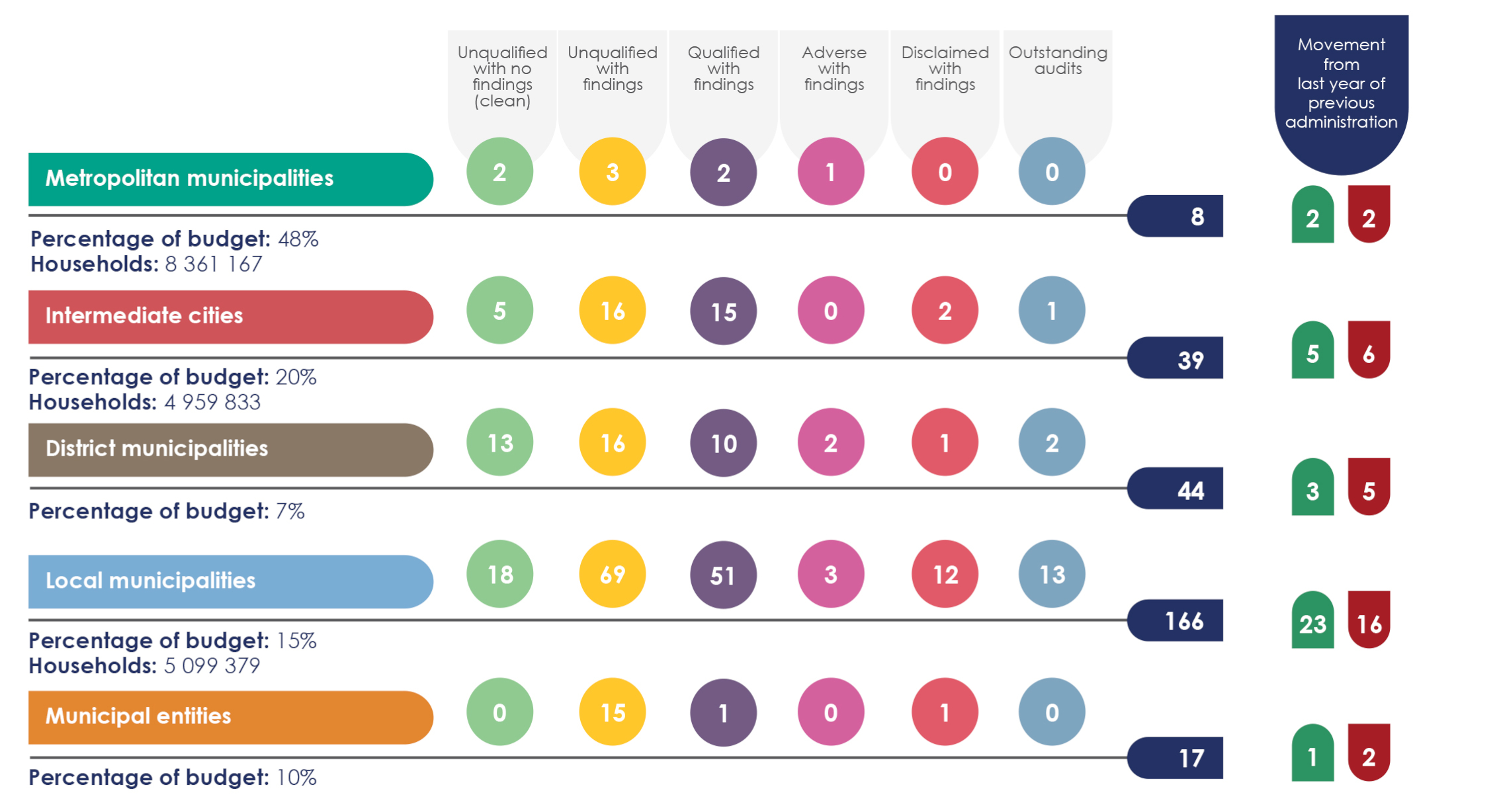

Local government audit outcomes

Local government is the sphere of government that is closest to our citizens because it provides basic services to the areas in which they live, and so directly impacts their lives.

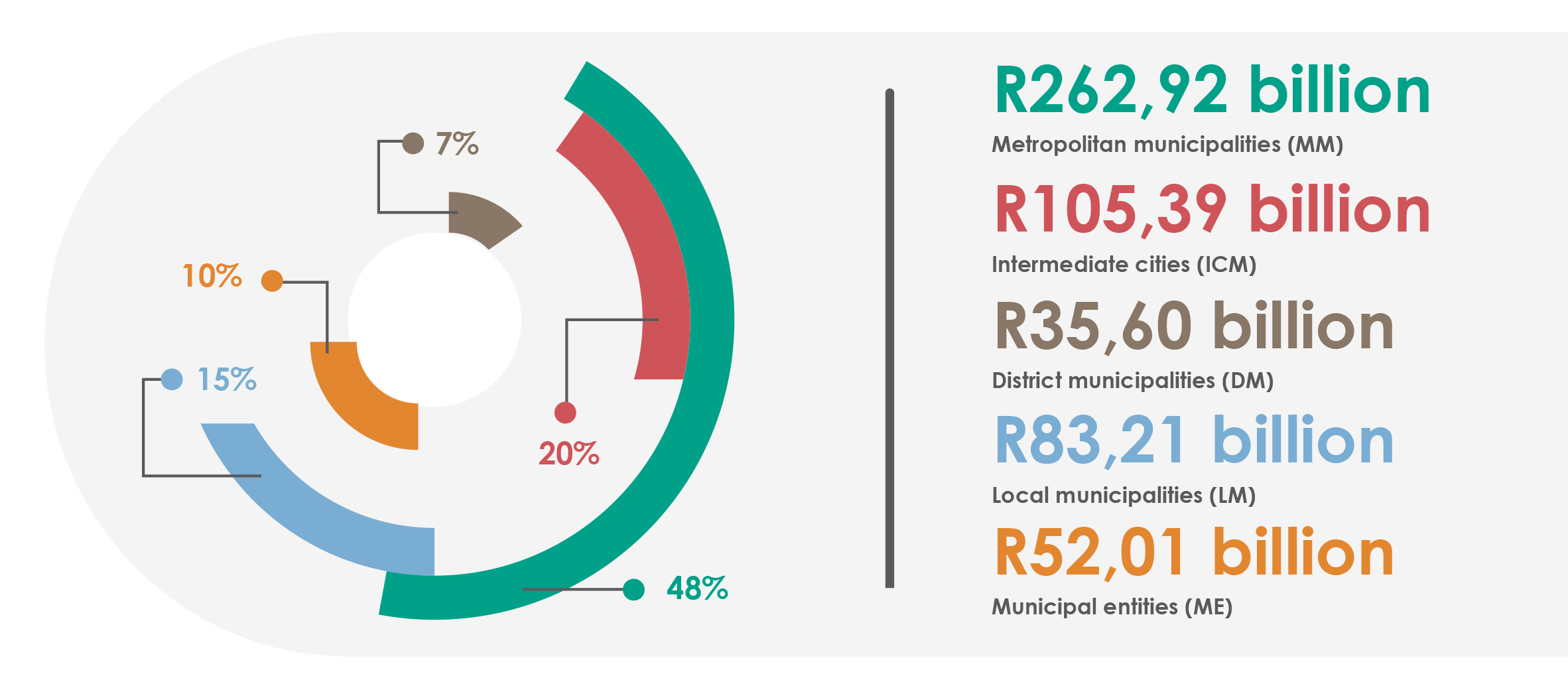

Metropolitan municipalities

commonly known as ‘metros’, are large urban complexes with populations of more than one million people. They account for the largest portion of municipal expenditure and serve the highest number of households and thus most of the people in the country.

Intermediate cities

are municipalities with large budgets that also serve a substantial number of households. They are responsible for all municipal functions not assigned to the district – in particular, local service delivery.

District municipalities

perform certain functions on behalf of local municipalities, such as integrated planning, infrastructure development, electricity provision and public transport. A district municipality may be a water services authority and may also provide financial, technical and administrative support services to a local municipality within its area as far as it can.

Local municipalities

can be large towns, small towns or rural areas. Just like intermediate cities, they are responsible for all municipal functions not assigned to the district, particularly service delivery to the residents in their designated geographical area. These municipal functions include water and sanitation services, electricity supply, refuse removal and road maintenance.

Municipal entities

are independent entities that perform municipal services on behalf of a municipality. Their financial statements are consolidated into those of their parent municipalities. Their audit outcomes are also important as they are responsible for a significant portion of municipal expenditure and service delivery programmes.

While we are encouraged by the strides made to improve the audit outcomes of municipalities, most notably the reduction of municipalities in the disclaimer category, it nevertheless remains disheartening to report ongoing failures in accountability and performance at municipalities.

While there were fewer municipalities with disclaimed opinions, there were also fewer clean audits. The audit outcomes showed an overall stagnation or little improvement.

Improved audit outcomes or action taken towards resolving long-standing issues were mostly due to deliberate steps by municipalities to improve and strengthen their internal control environments and through the support and intervention of coordinating institutions. The material irregularity process also triggered actions such as the submission of financial statements that were previously outstanding.

Our general reports included a particular focus on service delivery with a significant shift in the way we wrote and positioned these messages. Along with key recommendations and commitments, the insight into the impact of these results are meant to stimulate understanding and discourse to encourage a shift in culture.

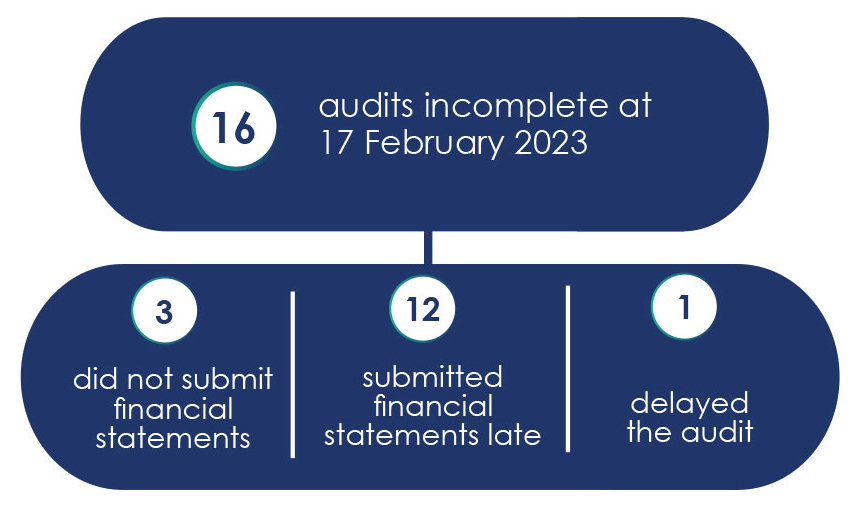

Audits outstanding

Our tailored audit insight:

- Published the water sector report and the Postbank cybersecurity report

- Engaged on different platforms regarding sector reports, e.g. at GIBS, and the infrastructure-built anti-corruption forum

- Issued the report on the rehabilitation of derelict and ownerless mines, which impacted the lived realities of the citizens by indicating the possible health and safety concerns for local communities around these mines

- Used PowerBI for enhanced data analytics and to identify key risks

Planning for impact

Using multidisciplinary teams on audits has become our best practice in delivering tailored audit insight to stakeholders. Multidisciplinary teams harness a diversity of skills and expertise to achieve complex audit objectives and gain a deep understanding of our auditees’ businesses. This assists them in navigating the complexities of an environment associated with high expenditure and greater audit risk.

Multidisciplinary teams include professionals in information technology governance, risks and controls systems, data analytics, information security, financial fraud and investigations, and in key government sectors including health professionals, economists, education specialists and engineers.

Their contribution to audit risk assessment, fraud data analytics and specialised auditee knowledge added comprehensive audit insight and improved audit efficiencies and effectiveness.

Data analytics

Audit analytics is fully integrated into the regularity audits as each audit is planned by an integrated team and data analytics opportunities are explored as part of the audit strategy. The audit planning meetings have become much richer; in the next financial year, we will be attempting to assess the extracted audit efficiencies resulting from the integrated planning.

While the use of computer assisted audit techniques (Caats) analytical procedures has been fully adopted across all our audits, due to limited capacity and capabilities, a phased-in approach has been adopted to scale up the use of PowerBI dashboards. These dashboards visualise an auditee’s business in a succinct and complete way thus serving as a risk identification tool. This year we relied on external specialists to fully implement advanced analytics and to upskill our internal resources.

Data analytics tools

The success of audit data analytics is strongly dependent on the use of appropriate tools. We acquired a number of software licences for a tool that proved to be valuable in transforming and analysing vast volumes of data and enables us to perform more advanced analytics, including machine learning, enhanced spatial analysis and text mining.

The process of acquiring a specialised media monitoring tool is at an advanced stage. The tool will assist us in conducting real-time media and social media scanning in support of our audit risk analyses.

Increase our impact on the accountability culture of the public sector by extracting unique insights and incorporating these into our products

The OYAP serves as a tool to demonstrate our impact and relevance to citizens while affirming that we have heard their concerns and are appropriately responding to their lived experiences.

Data analytics benefits:

- identifying fraud risk and reporting it

- ingesting data analytics in an assessment of government projects to close the gap between audit outcomes and service delivery

- predicting potential material irregularities and supporting evidence for them

- driving integrated messaging

- driving business decisions

The integrated one-year audit plan (OYAP) was developed using insight from integrated environmental scanning information and the audit risk register to:

- determine the audit themes

- identify the required AGSA tools and levers that will enable audit execution

- highlight the key institutions and clusters where work will be undertaken

Data analytics strategy

Information is one of the major assets of the AGSA. As the amount of data generated by the public sector continues to grow, the importance of leveraging the collected data to improve the AGSA’s capabilities for decisionmaking and analysis becomes critical. We conceptualised our approach towards the use of data analytics under one integrated strategy.

Stemming from the culture shift charter, the OYAP directs how we plan and carry out our audits to amplify a culture shift. It ensures that our audit work responds promptly to changing environments and emerging risks, while also being tailored to our internal priorities. In March 2023, exco approved the OYAP for 2023-24. As these audits are retroactive, this plan will be used when we audit the 2022-23 cycle.

The OYAP does not negate our mandated regulatory audits at national, provincial and local government, but rather elevates key matters that the audit portfolio must undertake in the respective cycles to foster and drive a culture shift.

It will also assist to approach our auditing in a more structured manner, resulting in efficiencies and an important straight point when deciding what to audit.

Real-time audits’ impact on the public sector accountability culture

During the reporting period we received a request to conduct a real-time audit on the use of the funds allocated for relief of damages caused by the floods in KwaZulu-Natal and the Eastern Cape.

The accumulated know-how from this audit is immense. Without prior experience and a methodology on auditing flood-relief funds, and not being able to draw on any specialist knowledge from private audit firms, our audit team conceptualised and conducted the audit with only our existing resources.

As part of our intention to interact with other roleplayers in society, we engaged with local civil society organisations to improve our risk identification and risk response. An important factor for this audit was to approach it considering the perspective of those that were ultimately impacted by this disaster i.e. the people on the ground. Our audit team visited the flood-damaged areas for better perspective of the audit risks and scope.

A special audit report that dealt with the immediate activities of the disaster relief was released and provided the public with insight on the response to the disaster. However, based on the slow rate at which funds were used, the auditor-general decided that we would audit this matter further during our annual audit. The respective provincial summaries in the general report on local government provided further insight on these realtime audits. Our insight elicited an admission by government that it was ill-prepared to manage disasters, and it provided commitments that we monitor on an ongoing basis.

Extensive interactions with all our stakeholders gave our reports the necessary attention and influence to compel action. Irregular contracts were stopped, payments to suppliers were withheld until the work was completed, prices were negotiated, and other measures were put in place to minimise leakage and maximise the use of public funds on actual disaster relief for the people affected by the floods. We are formalising a more controlled and structured approach to such real-time audits.

Differentiated audit approach’s impact on the public sector accountability culture

The differentiated audit methodology (DAM) project began in 2021-22 with three new methodologies:

- financial statements review

- audit of performance objectives (AoPO) findings engagement

- compliance findings engagement.

The objective was to provide an expanded menu of methodologies that can be applied to different categories of auditees, creating opportunities for efficiencies and a simpler audit process for specific auditees.

The project’s main phase (pilot and implementation approval) was completed in 2022-23 with all targets met.

The pilots showed significant efficiencies in all spheres of our audits with no negative impact on the outcome and messaging and 100% approval ratings from pilot teams.

Lessons learnt from the pilots allowed us to fine-tune the methodologies, include a gap analysis and determine how the gaps will be closed.

We supported our audit teams by supplying training on all three new methodologies and developing:

- a working paper to assess suitability of the institution being audited for the DAM project

- a toolkit to enable discussions with these institutions, and

- an approval process.

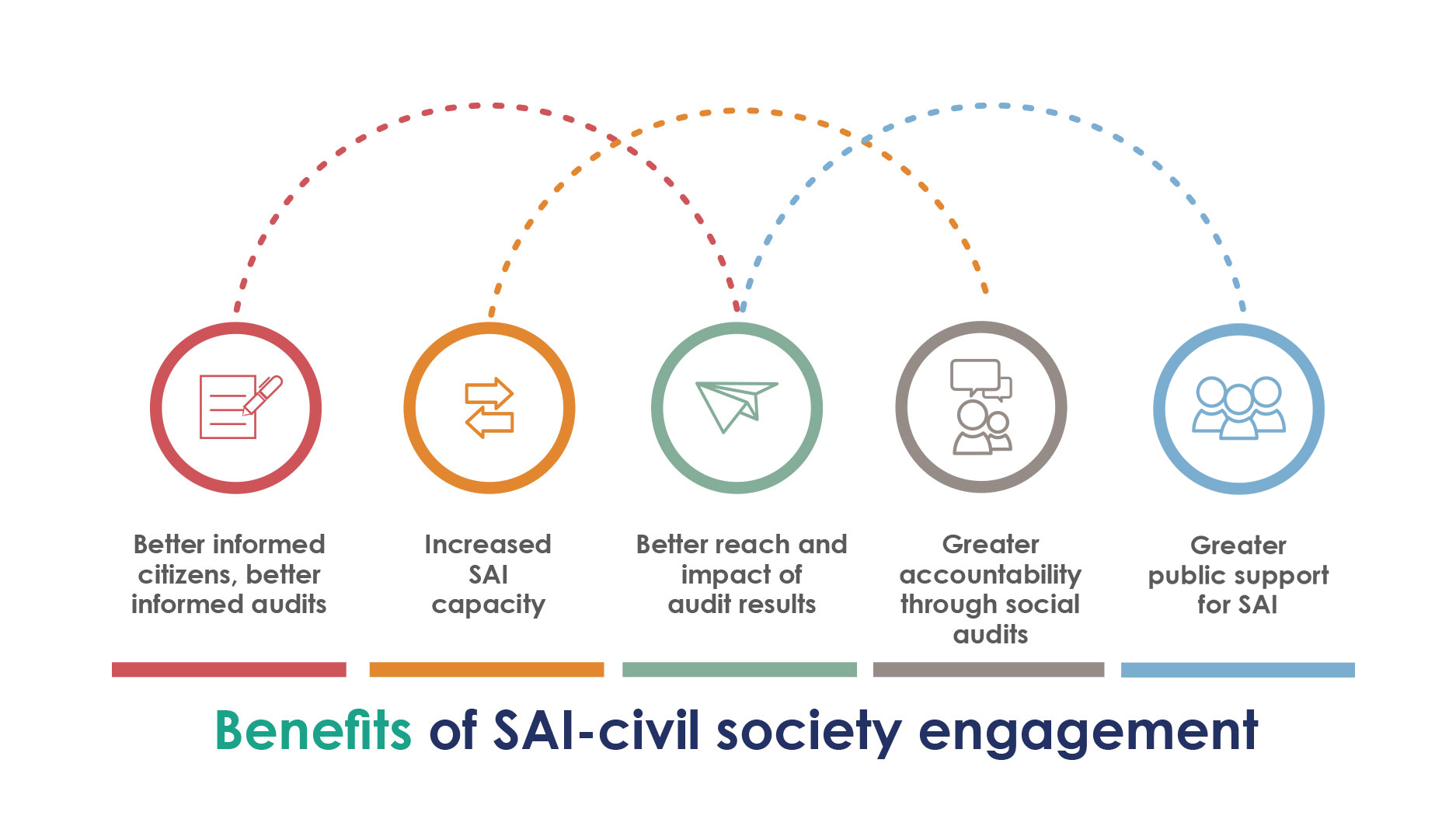

Our collaboration with CSOs and its impact on public sector accountability culture

The cornerstone of South Africa’s constitutional democracy is the Bill of Rights. In pursuit of strengthening democracy, we, in our unique way give effect to the fundamental human rights entrenched in chapter 2 of the Constitution. The missions of most CSOs are in some way linked to basic human rights. They are therefore ideally positioned to feed insight about basic human rights, citizen experiences and service delivery expectations into our audit work.

While we originally intended to manage our relationships with CSOs at an institutional or sector level, it is now clear that there is a need to institutionalise these relationships at a business unit and engagement level. To do so, we developed a streamlined framework for collaboration with the CSOs:

Most of the objectives saw good traction during the year:

- Basic processes to identify CSOs for engagement at BU level and a basic reporting functionality to keep track of the engagement were used throughout the year

- Basic use of CSO insight as inputs into the audit cycle planning processes (environmental scanning and risk assessment) worked well

- Using CSO insight on sector work was fully implemented. The work was also used to inform the related messaging (including standalone performance audit work) – main examples of this were using CSO insight in the flood relief audit processes and on the metro financial health, indigent debt and equitable share analysis

- An enabling toolkit to support the work of the CSOs was made available and enhanced as needs evolved

Overall, we are very satisfied with the progress we made in this aspect of work.

Leveraging the work of the commission into state capture

In the prior year, we reported on our interest in the investigative work of the Judicial Commission of Inquiry into State Capture, led by Chief Justice Raymond Zondo, as it has direct relevance to our audit work. The commission’s report highlighted the role of the public sector auditor in identifying and preventing fraud, corruption and other forms of impropriety.

Once the commission’s report was published, we launched a project to analyse the observations, findings and recommendations of the commission, which culminated in our own report to the President of the Republic. We made a number of commitments which we since have factored into our audit work to enable the audit teams to have a better line of sight of the indicators of capture.

Conclusion

We used all our intellectual resources to deliver insight that is relevant, actionable and focused on improving lives of ordinary South Africans.

While comprehensive audit plans have always been in place, we have now begun to align our audits with a long-term plan to ensure relevance, consistency and continuity of audit messages, to demonstrate transparency of our choices, and to allocate limited organisational resources to auditing what matters and what will have an impact on service delivery as the vehicle to improving lives of people.